People have been predicting the end of progress for as long as progress has existed.

In 1830, historian Thomas Macaulay posed a question that still resonates today. If everything behind us shows improvement, why do we assume everything ahead will get worse? A century later, economist John Maynard Keynes observed the same pattern. Despite remarkable gains in living standards, people remained convinced the best days were already behind them.

Today, that pattern appears to be repeating itself. Artificial intelligence has become a common source of both optimism and skepticism in 2026, and that uncertainty appears to be showing up in how some investors and professionals are thinking about their financial futures. For executives and corporate professionals navigating an already complex financial picture, the noise around AI may feel difficult to separate from what actually matters for long-term planning.

What Some Data Shows

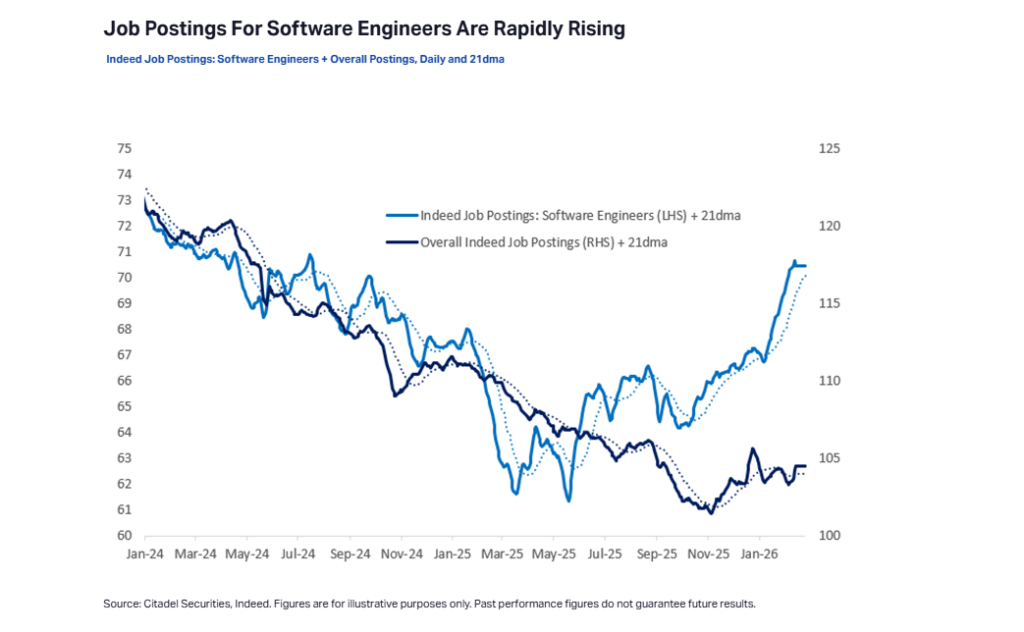

In February 2026, Citadel Securities published a detailed macro analysis responding directly to widespread market anxiety that had briefly unsettled equities earlier that month. The Citadel report, titled “The 2026 Global Intelligence Crisis,” examined current labor market data alongside historical patterns of technological adoption.

The findings were grounding. Job postings for software engineers were rising, up 11% year over year. Citing Federal Reserve data on AI adoption at work, Citadel surmised there is “little evidence of imminent displacement risk.” And the broader pattern of technological diffusion, the rate at which new technologies actually spread through an economy, has historically followed what researchers call an S-curve. Early adoption is slow and expensive. Growth accelerates as costs fall and infrastructure develops. Saturation eventually sets in.

In other words, it appears the timeline for AI to fundamentally reshape the labor market, as other technologies have, may be slower than the headlines suggest.

That does not mean change is not coming. It may indicate that the pace of that change could give individuals, businesses, and financial plans time to adapt.

Why This Pattern Is Not New

Farm automation, the railroads, electrification, the internal combustion engine, computers, and the internet. Each of these innovations arrived with serious warnings about widespread job loss and economic disruption. Some jobs did disappear. New industries emerged. Overall, employment and living standards expanded.

Keynes himself believed that technological progress would eventually reduce the workweek to 15 hours. He was correct about productivity. He was wrong about what people would do with it. Rising productivity lowered costs, expanded what consumers could afford, and created entirely new categories of work and spending that did not previously exist.

As Citadel’s analysis noted, AI-driven automation functions as a productivity shock. Productivity shocks lower marginal costs, expand potential output, and increase real income. They do not, in isolation, cause aggregate demand to collapse.

That is an important distinction for anyone making long-term financial decisions based on what they are reading in the news today.

What This Could Mean for Your Financial Plan

For some executives and corporate professionals, AI uncertainty tends to surface across various aspects of planning.

Equity compensation is one of them. Professionals holding restricted stock units or stock options in technology-adjacent companies are closely watching sector volatility. Concentration in a single employer’s stock, combined with uncertainty about that sector’s long-term trajectory, may warrant a careful review of how those positions fit into the broader portfolio.

Either decision, when made reactively, may not align with what the underlying financial plan actually supports. Understanding what your numbers say, independent of the current narrative, may help inform that decision more clearly.

None of these considerations requires predicting exactly how AI will reshape any specific industry. But they may warrant an honest look at your portfolio for concentrated risk exposure or a dependency on a given stock, and whether the plan is broadly diversified to help mitigate disruption regardless of its source.

The Investor’s Perspective

Historically, markets have a long history of pricing in uncertainty before that uncertainty resolves. The S&P 500 has experienced meaningful volatility in 2026, and some of that volatility reflects uncertainty about how AI will affect corporate earnings, labor costs, and productivity over the next several years.

The question worth asking is not whether AI will change things. It will. The question is whether your current financial plan is built to handle change, in whatever form it arrives.

A Note on Tax Considerations

For professionals with equity compensation, deferred income, or significant investment positions, changes in employment circumstances or income timing can carry meaningful tax implications. The interaction between ordinary income, capital gains, and retirement account distributions deserves careful review in the context of any career or planning transition.

Always consult with your tax professional when implementing any new tax strategy.

Next Steps

At LightForce Financial, we work with executives and corporate professionals who are navigating transitions, whether those transitions involve a career change, a relocation, an approaching retirement, or simply a financial picture that has grown more complex over time.

If questions about AI, market volatility, or your long-term financial plan have come up for you recently, we would be happy to walk through your situation during a complimentary consultation.

Source: Citadel Securities, “The 2026 Global Intelligence Crisis,” February 2026 — https://www.citadelsecurities.com/news-and-insights/2026-global-intelligence-crisis/